The Motorist Guide to used car buying in Malaysia

Let's be honest , buying a used car in Malaysia is exciting and terrifying at the same time. The excitement comes from the deal: a well-maintained second-hand car can save you RM30,000 to RM60,000 compared to buying new. The terror comes from not knowing what you are actually getting.

Faulty gear shifts. Hidden accident damage. A car that is still technically owned by a bank. These are real things that happen to real buyers in Malaysia every single year, not because they were careless, but because nobody told them what to look for.

This guide fixes that. Whether you are a fresh grad buying your first car or someone upgrading after years of driving a Kancil, you will find everything here: how to check a car's background, what to look for during an inspection, and, most importantly, how to figure out exactly what loan you can afford before you fall in love with a car you cannot realistically pay for.

Quick answer: Before you hand over a single ringgit, run a JPJ and CTOS check, get the car inspected at a Puspakom-certified workshop, and work out your loan eligibility using the DSR method. These three steps alone will protect you from most of the mistakes that cost Malaysian buyers dearly.

Understanding what kind of used car seller you are dealing with

Not all used car sellers in Malaysia are the same, and the type of seller you buy from changes everything about how you approach the process.

Private sellers, usually offer the lowest prices because they are not running a business. There is no middleman, no showroom overhead, no commission. But there is also no warranty, no comeback if something goes wrong, and no obligation for them to disclose defects they know about. Buying privately means more risk, but more room to negotiate.

Independent used car dealers occupy the middle ground. The better ones have reputations to protect and will offer short warranties or at least a cooling-off period. The not-so-good ones will tell you whatever it takes to get you to sign. Asking around in local Facebook groups or Lowyat forums for dealer reviews before you visit is genuinely useful.

Certified pre-owned (CPO) programmes run by Perodua, Honda, Toyota, and others sit at the premium end. These cars go through a manufacturer-approved inspection checklist, come with limited warranties, and are usually priced closer to new. You pay more, but you sleep better. For someone who does not want the stress of the full due-diligence process, a CPO vehicle is worth considering.

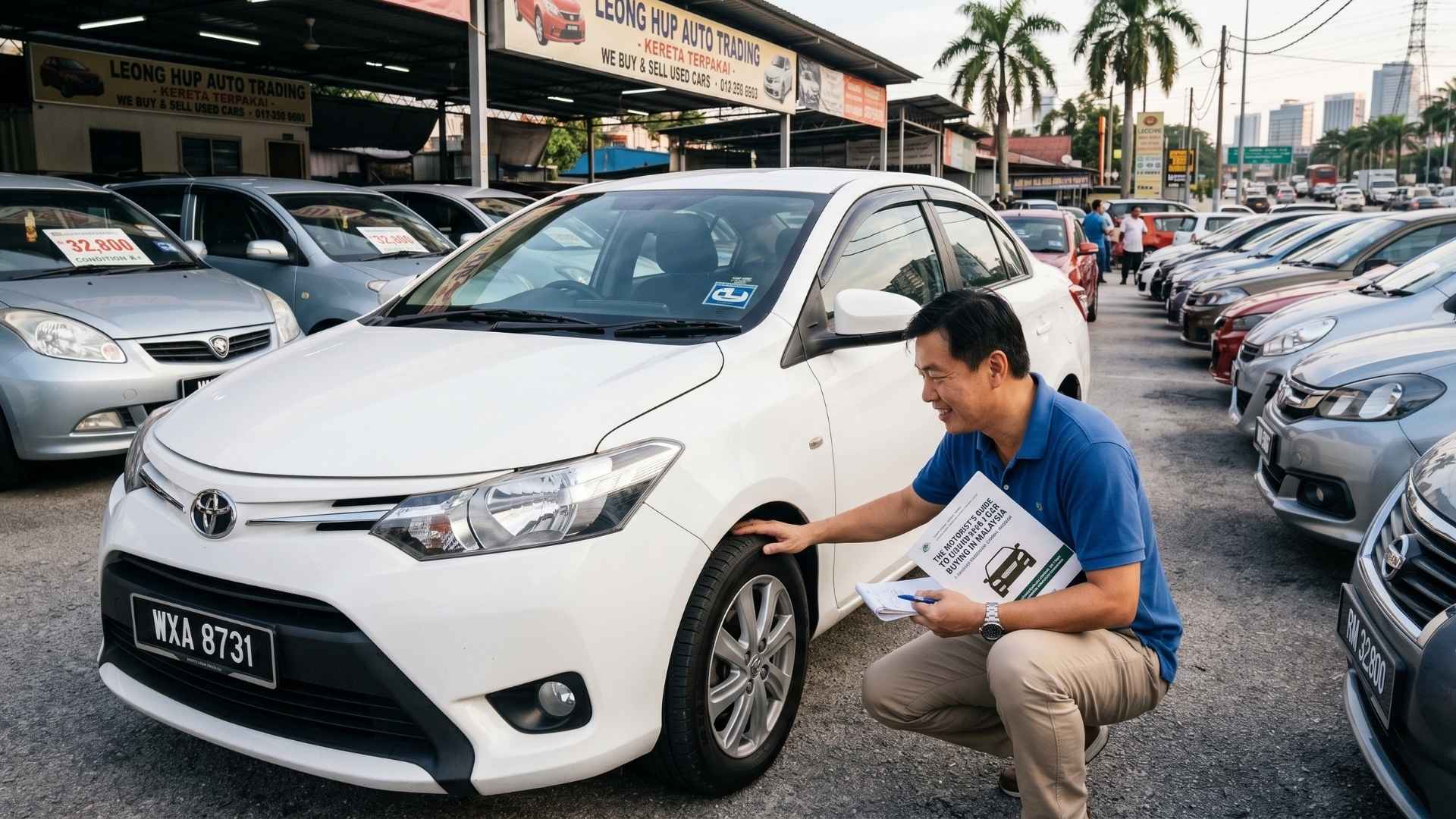

How to check a used car before you buy it

This is the part where most buyers either skip steps because they trust the seller, or feel too embarrassed to ask for documentation. Do not be that person. A seller who gets offended when you ask for paperwork is a seller who has something to hide.

Step 1: Check the JPJ records yourself

The Road Transport Department (JPJ) keeps a record of every registered vehicle in Malaysia. Before you agree to anything, get the vehicle identification number (VIN) and registration plate from the seller, then run a check through myEG.com.my or the JPJ portal. This tells you who legally owns the car right now, whether it has been reported stolen, and whether there is any outstanding road tax. Unpaid summonses, and some cars have thousands of ringgit worth of them, follow the car, not the driver. Make it a condition of the sale that all outstanding summonses are cleared before handover.

Step 2: Find out if the car is still under a bank loan

This one is important. If the seller still has an active hire-purchase loan on the car, the bank technically has a claim on it. Ownership cannot legally transfer until that loan is either fully settled or the bank releases the car. Ask the seller to show you a settlement letter from their financier, or a letter confirming the outstanding redemption amount. A trustworthy seller will have this ready. If they get evasive, walk away.

Step 3: Book your own Puspakom B5 inspection

Puspakom is Malaysia's official vehicle inspection body, and a B5 inspection is the most thorough check they offer, covering the chassis, bodywork, engine, suspension, and safety systems. It costs around RM140 to RM160 and takes about two hours. The critical word there is your own. Never accept a Puspakom report handed to you by the seller. Book it yourself, attend in person, and ask the inspector to walk you through what they found. A report flagging structural chassis damage, flood markers, or major accident repairs is not just bad news. It is leverage to renegotiate the price or leave entirely.

Step 4: Go through the service history properly

A car with a complete, stamped service booklet is worth more than the same car without one. Consistent servicing, especially at the correct mileage intervals, tells you the previous owner actually maintained the car. Gaps at 10,000 km, 20,000 km, or 40,000 km intervals are worth asking about. For Perodua and Proton vehicles, service centres can sometimes pull up a digital record using the VIN if the physical booklet is missing.

Step 5: Drive it like you mean it

A test drive around the block is nearly useless. Take the car onto a highway and push it past 80 km/h. Does the steering pull left or right? Does it vibrate through the wheel or the seat? Apply the brakes firmly at moderate speed on a clear road. Does the car stop straight? Turn on the air-con at full blast, drive for 20 minutes, and keep an eye on the engine temperature gauge. Listen for any knocking, grinding, or rattling when you accelerate, brake, or go over a bump. If the seller tries to limit what you can do during the test drive, that tells you something.

How to calculate your used car loan in Malaysia

Here is where a lot of buyers go wrong. They find a car they love, agree on a price, then go to the bank and discover they cannot actually afford the loan they were hoping for. Working this out before you start shopping saves you from a painful conversation and from making an emotional decision with money you do not have.

What is DSR and why does it matter?

Malaysian banks use something called the debt service ratio, or DSR, to decide whether to approve your loan and how much to give you. DSR is simply the percentage of your gross monthly income that goes toward debt repayments. Most banks in Malaysia will not approve a loan if your DSR goes above 60 to 70 percent. Some set the limit lower depending on your income bracket.

DSR (%) = (Total monthly debt commitments ÷ Gross monthly income) × 100

Your total monthly debt commitments include everything: your existing car loan if you have one, PTPTN, housing loan, credit card minimum payments, and the new instalment you are applying for. Add them all up, divide by your gross salary, multiply by 100. If the result is above 60 to 70 percent, the bank will likely say no, or offer you a smaller amount.

How used car loan interest works in Malaysia

This is something a lot of people do not realise until they are already committed: Malaysian hire-purchase loans use a flat interest rate, not a reducing balance rate. With a flat rate, interest is calculated on the full original loan amount for the entire duration of the loan, not on the outstanding balance as you pay it down. This means you pay more total interest than you might expect.

Monthly instalment = (Loan amount + Total flat interest) ÷ Total number of months

Total flat interest = Loan amount × flat interest rate × loan tenure in years

Here is a real example. Say you borrow RM40,000 at a flat rate of 3.5% per annum over 7 years. Your total flat interest is RM40,000 × 3.5% × 7 = RM9,800. Add that to the principal: RM40,000 + RM9,800 = RM49,800 total repayable. Divide by 84 months, and your monthly instalment is about RM593. That is the number you need to check against your DSR.

Calculating your loan step by step

Step 1: Know your down payment

Used car loans in Malaysia typically cover between 70 and 90 percent of the car's value, depending on the car's age and the lender's policy. Cars older than five years are usually capped at 70 percent financing. So on a RM50,000 car financed at 80 percent, you need RM10,000 upfront. Have this number nailed down before you negotiate, because it affects everything else.

Step 2: Find out the interest rate you qualify for

Used car hire-purchase interest rates in Malaysia currently range from around 2.8 to 4.5 percent per annum, depending on the lender, your credit score, and the vehicle's age. Older cars attract higher rates. Get indicative rates from at least two or three banks before you commit to anything. Better yet, use a loan comparison tool so you can see the spread without spending an afternoon calling banks.

Step 3: Decide on your tenure

Used car loans in Malaysia are generally capped at seven to nine years depending on the car's age. A longer tenure means a lower monthly payment but significantly more total interest paid. Run the numbers for five years, seven years, and nine years side by side. The difference in total interest between a five-year and a nine-year loan on a RM40,000 borrowing can easily exceed RM5,000. That is real money.

Step 4: Apply the formula and check against your DSR

Take your loan amount, multiply by the flat rate, multiply by the tenure in years to get your total interest. Add that to the loan amount. Divide by the total number of months. That is your monthly instalment. Plug that into your DSR calculation alongside your other debt commitments and your gross income. If the DSR stays below 60 percent, you are likely in safe territory for a bank approval.

Step 5: Do not forget the costs beyond the instalment

Your actual monthly cost of owning the car is higher than just the instalment. Road tax for a 1.5-litre car runs around RM90 a year. Comprehensive insurance for a used car typically falls between RM1,000 and RM2,500 annually depending on the car's value and your NCD. Budget for at least one service every three months at roughly RM150 to RM300 per visit. Add all of this up and divide by 12 to get your real total monthly car cost. Then ask yourself honestly whether it fits your life.

Transferring ownership: what happens at JPJ

Once the price is agreed and the seller has cleared their loan, you complete the ownership transfer at a JPJ branch. Both buyer and seller need to be there in person, along with both ICs, the vehicle registration card (geran), a signed sale and purchase agreement, and the Puspakom B5 report if the car's age requires it. The transfer fee itself is small. The process takes most of a morning depending on the branch and how busy it is.

Some dealers offer to handle the transfer through a runner for a service fee of RM200 to RM500. It is convenient, but make sure you understand exactly what documents are being submitted on your behalf. Attending in person gives you certainty that the transfer is done correctly and that you walk out as the legal owner on the same day.

Let Motorist Malaysia take some of the stress out of this

Look, buying a used car in Malaysia does not have to feel like defusing a bomb. It just requires the right information and the right tools, and that is exactly what Motorist Malaysia was built for.

From verified used car listings and free car valuations to practical ownership guides written for Malaysian drivers, Motorist Malaysia gives you what you need to walk into any negotiation with confidence. Whether you are trying to figure out what a fair asking price is, comparing loan options across lenders, or just trying to understand what a Puspakom report actually means, it is all there.

Head over to motorist.my to explore used car listings, check what your target car is really worth, and access tools built specifically for Malaysian buyers. No jargon. No runaround.

Frequently asked questions

1. How do I know if a used car has been in a flood?

The signs are there if you know where to look. A musty or mildewed smell inside the cabin is one of the most telling. Check under the dashboard for corrosion on electrical connectors, look at the spare tyre well for sand or silt, and inspect the undercarriage and wheel arches for rust that does not match the car's age. A Puspakom B5 will flag structural corrosion, but having an independent mechanic do their own check is always worth doing as well.

2. Can I still get a used car loan if my credit score is not great?

Yes, but it gets harder and more expensive. Banks in Malaysia use your CCRIS and CTOS records to assess lending risk. A low score, usually from missed payments or high existing debt, means banks may offer less financing, require a bigger down payment, or charge a higher interest rate. Some finance companies specialise in higher-risk applicants, but their rates reflect that. The most practical approaches are to reduce your existing debt before applying, or to offer a larger down payment to reduce what the bank has to lend you.

3. What age of used car is the best buy in Malaysia?

Cars between three and five years old tend to offer the best combination of value and reliability. They have already absorbed the sharpest depreciation from new, are usually still reliable, and are generally still eligible for up to nine-year hire-purchase financing. Cars older than ten years can look attractive on price, but financing becomes harder to get, insurance costs often rise, and maintenance expenses start to climb in ways that are difficult to predict.

4. How much should I actually budget for a used car in Malaysia?

Beyond the purchase price, factor in a buffer of around 10 percent for any immediate repairs or maintenance the car needs after purchase. Add insurance, road tax, and three months of instalments held in reserve as a financial cushion. As a general guideline, all of your car-related expenses combined, including instalment, insurance, road tax, and regular servicing, should ideally not exceed 15 to 20 percent of your monthly take-home pay.

Read More: https://www.motorist.my/article/5667/over-15m-vehicles-in-malaysia-with-road-tax-expired

I want to find the highest selling price for my car within 24 hours!

Download the Motorist App now. Designed by drivers for drivers, this all-in-one app lets you receive the latest traffic updates, gives you access to live traffic cameras, and helps you manage vehicle related matters.