Why Malaysians buy cars they cannot actually afford and pay for it for years

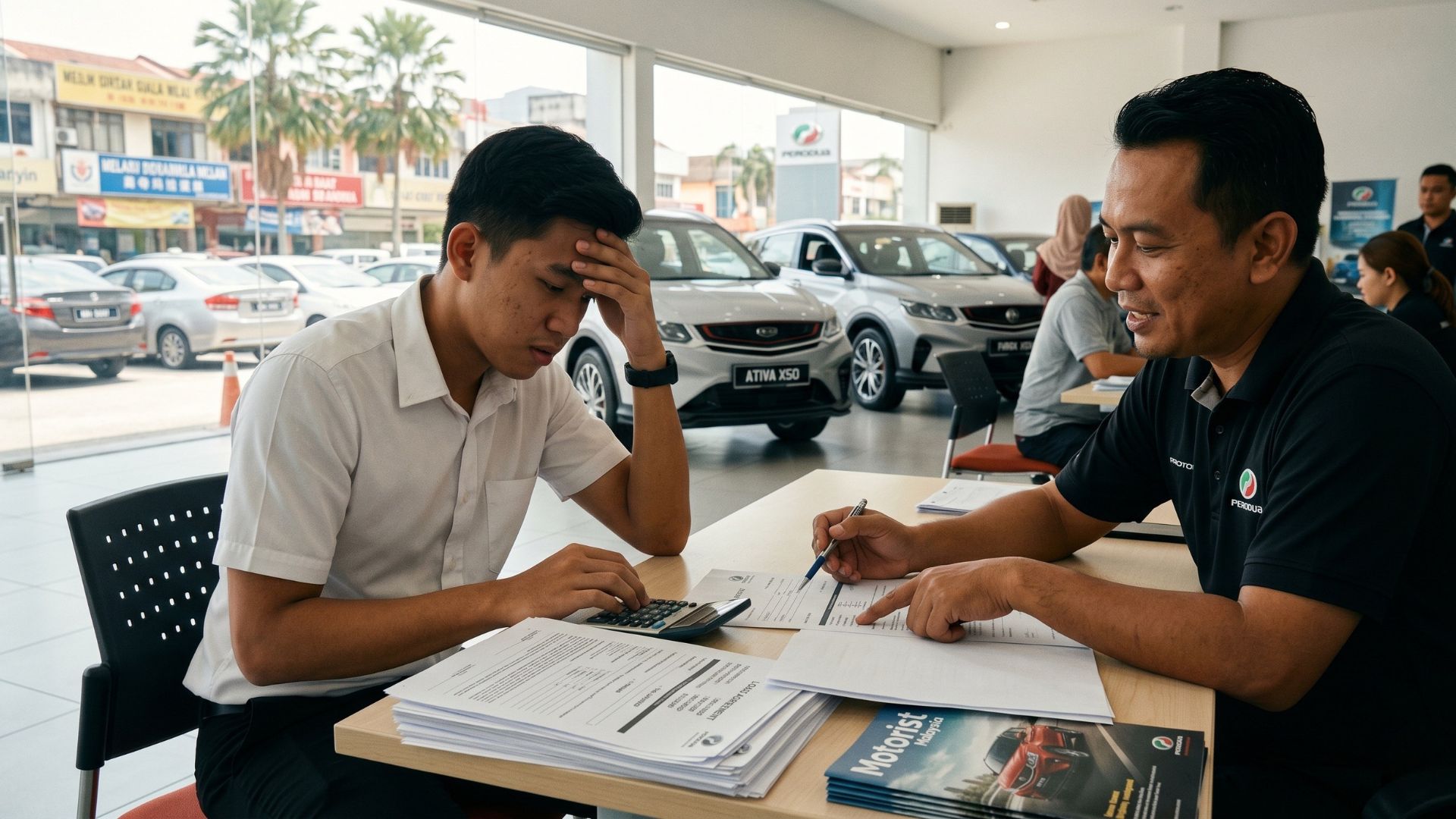

There is a scene that plays out across Malaysia every week. A fresh graduate earning RM3,000 a month walks into a showroom and walks out with a RM100,000 loan, a nine-year repayment schedule, and a monthly instalment that swallows more than a third of his salary before he has paid a single bill.

He is not foolish. He is doing exactly what most Malaysians around him are doing.

What "affordable" actually means

Car affordability is not about whether the bank said yes. Banks approve loans based on whether they think you will keep paying, and that is a completely different question from whether the loan is actually good for you.

Financial planners generally recommend that all vehicle-related costs combined including the monthly instalment, insurance, road tax, petrol and basic maintenance should not eat up more than 15 to 20 percent of your gross monthly income. For someone earning RM3,000, that works out to somewhere between RM450 and RM600 a month for everything car-related. A RM100,000 loan over nine years at 2.5 percent flat rate already produces a monthly instalment of around RM1,050 on its own. That is before you have filled the tank once.

The pressure nobody admits is there

Ask most Malaysians why they bought the car they did and they will tell you it was practical, reliable, good resale value. They will not say it was because their relatives kept asking when they were going to upgrade, or because turning up to a family gathering in a Kancil felt embarrassing after landing a corporate job.

But that pressure is real and it runs deep. In a culture where visible markers of progress matter, the car sitting in front of the house on Hari Raya is a statement. Choosing something modest when you are now earning a salary is often quietly read as not doing well enough. This is rarely said out loud. It does not need to be.

The salesperson in the showroom understands all of this better than you might expect. When they tell you the RM120,000 car is only RM1,100 a month, they are not lying. They are just making sure you are thinking about the monthly number and not the total number. Over nine years at 2.5 percent flat interest, a RM100,000 loan will cost you about RM122,500 in total repayments. The car will be worth perhaps RM20,000 to RM35,000 by the time you finish paying. The gap between those two figures is what the instalment illusion costs you.

What nine years actually looks like

Take a real scenario. Someone earns RM3,000 gross. After EPF contributions, take-home pay is around RM2,550. The car instalment is RM1,100. Petrol and toll easily add RM350. Rent in the Klang Valley takes at least RM600. Food and daily expenses run another RM400. That leaves roughly RM100 at the end of the month before anything unexpected happens.

A flat tyre is a crisis. A dental bill is a crisis. A family member needing help is a crisis. The credit card slowly becomes a coping mechanism rather than a convenience.

By the time the loan ends nearly a decade later, close to RM119,000 will have been paid for an asset worth a fraction of that. And the quieter cost is everything that money could not become. That same RM1,050 a month put into a unit trust returning 7 percent annually over nine years would have grown to around RM160,000. A house deposit. A business. A genuine financial cushion. Gone because the car had to say something about who you were at 24.

A more honest way to buy a car

The simplest rule is to take your gross monthly income and multiply it by 0.15. That is the most you should be spending on everything car-related each month. For a RM3,000 earner, the monthly instalment needs to be somewhere around RM300 to RM350 to stay within a healthy range. That points to a Perodua, a used compact or a well-kept national car. Not a status symbol. But something you actually own rather than something that owns you for the next nine years.

If you are already in a loan that feels too tight, even paying a small amount extra on the principal each month will reduce your total interest. If it has gone beyond tight and you are genuinely struggling, call your bank before you miss a payment. Most banks have restructuring options that are far less damaging than going into default.

Before you sign anything, check Motorist Malaysia

Motorist Malaysia is the platform serious car buyers use before they walk into a showroom. The car valuation tool shows you what any vehicle is actually worth in the current market so you are not negotiating blind. Insurance comparison tools let you find proper coverage without overpaying. And the used car marketplace has verified listings across every budget so you can find something that fits your finances rather than stretch them.

Visit motorist.my before you commit to anything. It takes ten minutes and could save you years.

FAQ

1.What percentage of my salary should go to a car loan in Malaysia?

All vehicle costs combined including instalment, insurance, road tax, petrol and maintenance should stay within 15 to 20 percent of your gross monthly income. The instalment alone should not exceed 10 to 15 percent. For someone earning RM3,000, that means keeping the monthly instalment below RM450.

2.Why do banks approve loans that seem too large for someone's income?

Banks assess whether you are likely to keep servicing the debt, not whether the loan is financially healthy for you. Getting approved means the bank is confident in repayment, not that the purchase is a good idea. Those are two entirely separate evaluations.

3.Is buying a used car smarter than buying new?

For most buyers on a typical Malaysian salary, yes. A car that is two to four years old has already taken the steepest depreciation hit. You get a significantly lower purchase price without giving up a reliable, well-maintained vehicle. The monthly commitment stays within a range that does not consume your entire budget.

4.How long should a car loan be?

Five years or fewer is what most financial planners recommend. Seven to nine year loans keep monthly payments low but the total interest you pay over the tenure is substantially higher, and you spend more of those years owing more than the car is worth. A shorter loan on a cheaper car is almost always a better deal than a longer loan on a more expensive one.

Read More: Love on four wheels: romantic drives in Kuala Lumpur

I want to find the highest selling price for my car within 24 hours!

Download the Motorist App now. Designed by drivers for drivers, this all-in-one app lets you receive the latest traffic updates, gives you access to live traffic cameras, and helps you manage vehicle related matters.