The 'negative equity' : selling your car when you still owe the bank (2026 Edition)

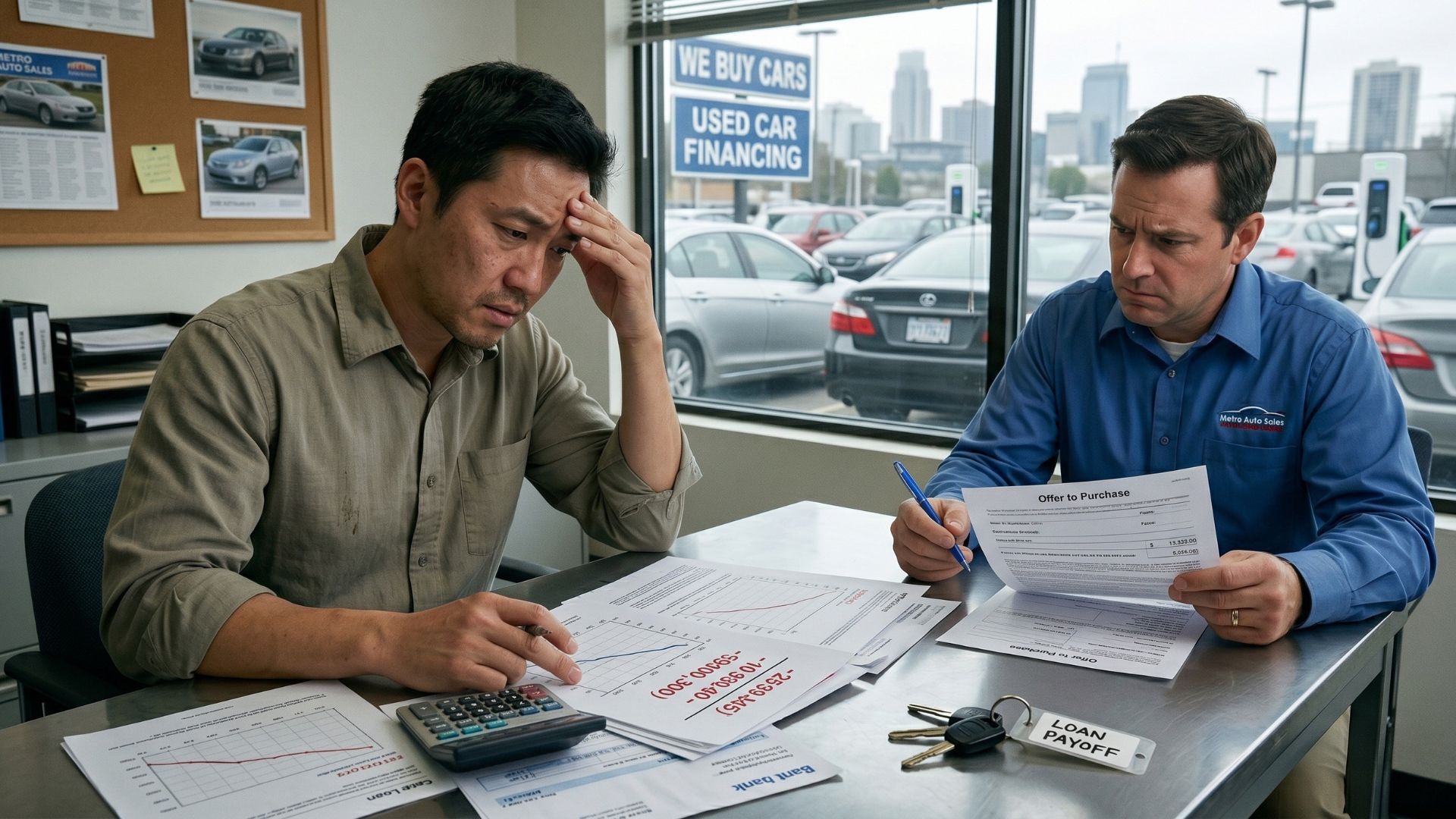

It is a common scenario in 2026: You’ve had your car for four years, you’re feeling the pinch of the floating RON95 fuel prices, and you want to downsize. You check your bank’s mobile app for the "Full Settlement" amount, then check the market value of your car, and your heart sinks.

You owe the bank RM55,000, but the highest offer you’ve received for the car is only RM45,000.

This RM10,000 gap is what experts call "Negative Equity." In Malaysia, where 9-year hire-purchase loans are the norm, thousands of motorists find themselves “underwater”, owing more to the bank than the asset is worth.

1. Why is Negative Equity So Common in Malaysia?

The Malaysian automotive market has specific factors that contribute to this debt trap:

The 9-Year Loan Trap: While long-term loans make monthly installments affordable, the car’s depreciation drops much faster than the principal amount of the loan in the first five years.

Rapid Depreciation of Certain Brands: While Perodua and Toyota hold value well, other brands may lose 40-50% of their value within the first three years.

Economic Shifts in 2026: With the removal of blanket fuel subsidies, high-displacement internal combustion engine (ICE) cars have seen their resale values dip as buyers flock to hybrids and EVs.

2. Step 1: Calculate the "Gap"

Before you can sell your car, you need the exact numbers. Do not guess.

Get Your Full Settlement Amount: Log into your bank portal (Maybank2u, CIMB Clicks, etc.) or call your hire-purchase department. Ask for the "e-Settlement" price valid for the next 10 days. This includes the remaining principal minus the "Rule of 78" interest rebate.

Get a Real-Time Market Valuation: Don't rely on old newspaper ads. Use Motorist Malaysia’s Free Valuation Tool to see what dealers are actually paying for your car today.

The Formula:

Full Settlement Amount - Market Value = Your Negative Equity (The Top-Up).

3. The Dangerous Trap: Why You Must Avoid "Sambung Bayar"

When faced with a RM10,000 top-up, many Malaysians are tempted by "Sambung Bayar" (Continue Payment). This is where you "sell" the car to a third party who promises to pay the monthly installments without changing the ownership at JPJ.

In 2026, this is more dangerous than ever:

It is Illegal: Under the Hire Purchase Act 1967, you cannot transfer a financed car without bank consent.

Legal Liability: If the new "owner" gets into an accident, commits a crime, or misses payments, you are legally responsible. The bank will sue you, and your CCRIS/CTOS score will be ruined.

No Recourse: If the car is "stolen" by the person you gave it to, insurance will not pay out because you breached the policy terms.

4. How to Fix Negative Equity: 3 Real Solutions

If you must sell your car but have negative equity, here are the professional ways to handle it:

Solution A: The Cash Top-Up (The Cleanest Break)

If you have savings, paying the difference is the best way to move on. Once you sell the car through a platform like Motorist, the dealer handles the settlement with your bank. You pay the dealer the "gap" amount, they pay the bank in full, and the ownership transfer (JPJ Tukar Nama) is completed via Biometric verification.

Solution B: Bridging with a Personal Loan

If you don't have the cash but need to stop the high monthly car installments, some motorists take a small personal loan to cover the RM10,000 gap. While this is still debt, a personal loan often has a lower monthly commitment than a heavy car loan, giving your monthly budget more "breathing room."

Solution C: "Rolling" the Debt (Trade-In)

Many used car dealers offer to "roll" your negative equity into the loan for your next car.

Example: You owe RM10k extra on your old car. You buy a cheaper used car for RM30k. The dealer tries to get you a loan for RM40k.

Warning: This is risky as it starts you off with even deeper negative equity on the second car.

5. How Motorist Malaysia Minimizes Your Negative Equity

The best way to reduce the "gap" is to get a higher price for your car. Traditional trade-ins at showrooms often give you the lowest price because the salesperson takes a commission.

Why sell through Motorist?

Higher Offers: We share your car details with over 500+ verified dealers across Malaysia. By creating a "bidding" environment, you get the absolute ceiling of the market price.

RM2,000 - RM5,000 Extra: Our users often find their offers are RM3,000 higher than a standard dealership trade-in. That’s RM3,000 less that you have to "top up" to the bank.

Hassle-Free Settlement: We guide you through the bank settlement process, ensuring the bank receives the funds and your loan is closed correctly.

6. Checklist for Selling a Financed Car in 2026

- Service History: Ensure your service book is updated. A car with full records fetches RM2k-RM3k more.

- Puspakom B5: Have your car inspected. A "Pass" report builds buyer confidence.

- Spare Keys & Manuals: Small items that prevent price "lowballing."

- Motorist Valuation: Get your Instant Quote to know your standing.

Frequently Asked Questions (FAQs) About Negative Equity

1. Can the bank refuse to let me sell my car if I have negative equity?

The bank cannot refuse the sale as long as the loan is paid off in full. If you can provide the "gap" amount in cash or via a secondary loan, the bank will issue the release letter once the settlement is received.

2. Does negative equity affect my credit score?

Not directly. However, if you fail to pay the "gap" and the car is repossessed, or if you fall behind on payments, your CCRIS/CTOS score will be negatively impacted. Selling the car and settling the loan actually improves your Debt Service Ratio (DSR).

3. Will my insurance refund help cover the negative equity?

Yes! When you sell your car and cancel your insurance policy, you are entitled to a pro-rated refund of the premium (if you haven't made a claim). This money can be used to offset your top-up amount.

4. Is it better to wait for the car's value to catch up to the loan?

In Malaysia, cars rarely appreciate. However, around year 7 of a 9-year loan, the principal usually starts to drop faster than the depreciation. If your gap is currently RM20,000, waiting another year might reduce it to RM10,000.

5. Can I transfer my car loan to another person?

Technically, this is called a "Loan Substitution," but Malaysian banks rarely approve this for individual hire-purchase agreements. The new buyer must usually apply for a fresh loan.

6. Does Motorist Malaysia charge me a fee to sell my car?

Motorist Malaysia provides a platform for you to receive bids from dealers. Our valuation service for car owners is free, and there is no obligation to accept the offer if you aren't satisfied.

7. What happens if I can't afford the "top-up" cash?

You may need to look at refinancing options or a personal loan. Alternatively, you can continue driving the car while making extra "capital repayments" (if your bank allows) to reduce the principal faster.

8. Why is my "Full Settlement" higher than my remaining installments?

It isn't. Due to the "Rule of 78," the bank gives you a rebate on the interest you haven't used yet. Your settlement figure will always be lower than the sum of your remaining monthly payments.

9. How do I know the dealer will actually pay the bank?

When selling through Motorist, we deal with verified, reputable dealers. The payment is usually made via a bank draft or direct transfer to your hire-purchase account, and the transfer is only finalized once the bank confirms receipt.

10. Can I sell a car that has been in an accident?

Yes, but expect higher negative equity. Accident history significantly lowers resale value. Disclosing this upfront on Motorist ensures you get an honest bid and avoids a "rejected" sale later during the physical inspection.

Negative equity is a financial hurdle, but it isn't a dead end. By understanding your settlement amount, avoiding illegal schemes like sambung bayar, and using a high-reach platform like Motorist Malaysia to maximize your sale price, you can clear your car debt and start fresh.

Don't let debt keep you stuck. Find out the true value of your car today and see how small your "gap" really is.

[Click here to get your Free Car Valuation from Motorist Malaysia now!]

Read More: Malaysia EV registrations up 58.5% in 2026: is it time to switch to electric?

I want to find the highest selling price for my car within 24 hours!

Download the Motorist App now. Designed by drivers for drivers, this all-in-one app lets you receive the latest traffic updates, gives you access to live traffic cameras, and helps you manage vehicle related matters.